The Greater Chennai Corporation (GCC) with 20 other corporations recently saw the conduct of municipal elections after a gap of 6 years. Since India advocates the theory of “Democracy at the grassroots level”, city governments play an important role in the governance structure. They are directly related to the daily life of the citizens.

The 12th Schedule of the 74th Constitutional Amendment Act (CAA), 1992 recognises the Indian Government Structure in 3 tiers: central, state and local. The 74th CAA devolves powers and functions to Urban Local Bodies (ULBs). This is done to enable them to function as the third tier of government. Therefore, it is essential to ensure that ‘City Governments’ act as ULBs and not merely as institutions for service delivery.

Importance of municipal finance

City governments play a vital role in service delivery. They are also engaged in regulating, developing, facilitating and collaborating for the growth of the urban area. To undertake service delivery and developmental projects in the city, adequate allocation of municipal finances for smooth functioning is necessary. City governments allocate expenses on a list of services. The ambit of services include transportation, policing, fire protection, water and sewers, garbage collection and disposal, education and social expenditures, housing, health, education, culture etc.

Establishing infrastructure for these services is also undertaken by the city government. According to the ‘principle of subsidiarity’ the efficient provision of services requires that decision-making be carried out by the level of government that is closest to the individual citizen. For example, a Councillor who is a resident of his or her own ward, can comprehend and solve a particular issue proficiently. Therefore, expenditure responsibilities should only be assigned to the same government.

Decentralization of governance

India is undergoing rapid urbanisation, the pace of which poses significant challenges to urban governance. Urban areas attract people to cities and towns which leads to a surge in population. It is estimated that, by 2030, more than 40 percent of the Indian population will be living in cities. But the question is: How urban is India really?

As per the 2011 census data, 31% of the country is ‘urban’. On the contrary the administrative and census definition undermines the transitions in urbanisation taking place in small cities and towns. It is extremely challenging to find a precise definition that could capture the true nature of all places. Therefore, it is essential to identify and resolve the flaws in the current method of defining urban areas. This plays a significant role in forming policies and government schemes.

This poses the question: Are local urban governance structures in India equipped to respond to the needs of their citizens and tackle future problems?

Devolution of powers

Government holds the responsibility to form policies, initiate reforms for the citizens and deliver services efficiently. The code of a democratic structure of government involves devolution of executive powers amongst the three tiers of the government. Each sphere should have autonomous powers and responsibilities. There must be no overlap of roles and responsibilities. But in the present governance structure, devolution of powers and functions remain far from what was stipulated. State Governments have not relinquished control. The reasons for this range from the inherent challenges with change management, to questions of power and where decision-making control resides.

Read more: Why does actor Rajinikanth pay less tax than Nagarajan of Nanganallur?

The city governments are responsible for delivery of 18 functions listed in the 12th Schedule. This includes water supply, roads and bridges, solid waste management, planning for economic and social development, vital statistics, public health, sanitation, public amenities.

The fact that City Governments do not have complete control over the 18 functions leads to issues in delivery of services. But the urban governance structure in India has not given the working powers to the city government due to multiple reasons. The City Governments need to be given independent decision-making authority. They must also ensure that they are accountable to the citizens.

Status of Fiscal Empowerment in Chennai

Praja Foundation (2021) studied different indicators on ‘Fiscal Empowerment’, analysing the financial strength of the city government and powers devolved to them. Out of 14 cities, Chennai was part of the study where financial devolution of Chennai was studied. Following are the indicators for Chennai were researched.

1. Data Availability

The study analysed the budget document/data and audit account statements available on the official website for the years 2017-18 to 2021-22 and 2016-17 to 2018-19 respectively. Greater Chennai Corporation (GCC) has all five budget documents published online, whereas the audit account statement for only 2017-18 and 2018-19 is available.

It is important to publish budget and audit documents in the public domain. City Governments need to be more transparent by publishing the budget and audit accounts on the city government website. Non-availability of budget documents in the public domain shows transparency failure of municipal accounting. Transparency in budget and audit documents can contribute towards better credit rating of the city government.

2. Governance Indicators

Article 243X of the 74th Constitution Amendment Act, 1992 has recommended State Governments to transfer powers to City Governments to assign and levy taxes and charges. City Governments should aim to be self-sustainable and independent in their functioning. Furthermore, State Governments should ensure that the constitutional principles are upheld in terms of financial empowerment of the City Governments.

For this to take place in its true spirit, the City Governments should be empowered with independent authority to perform the following: (i) Introduce new taxes and charges and (ii) Revise existing rates of taxes and charges being levied. City Governments should hold independent authority to allocate its financial resources, and also be able to independently approve budget.

| Indicators | GCC |

| Does the City Governments hold independent authority to revise the existing tax rates/charges as per State Municipal Act? | Yes |

| Does the City Governments hold independent authority to introduce new taxes/charges from the assigned list of taxes as per State Municipal Act? | Yes |

| Does the council have independent authority to approve the budget according to the State Municipal Act? | No |

| Does the State Municipal Act make it mandatory to publish the budget and accounts? | Yes |

| Does the State Municipal Act have a mandatory provision on external audit of Municipal accounts? | Yes |

| Does the City Governments publish its Credit Rating in the financial statements/budget/website? | No |

| Are the contracts and tenders dealt by the City Governments published on the City Govt. website? | Yes |

| Is accrual based double entry accounting system implemented by City Governments? | Yes |

| Does the City Govt. enclose the following: (1) Outcome/Performance Budget (2) Gender Inclusive Budget(3) Poverty Alleviation Budget (4) Ward wise budget estimates | No No No Yes |

The City Governments should be empowered to prepare and approve its own budgets. It is the City Government which can best represent the mandate of its citizens. This can be done through city level planning. Prioritising projects and schemes can be based on the financial resources available. Hence, City Governments should be allowed to hold independent authority to allocate its financial resources accordingly. It must also be able to independently approve budgets (which should be under the prerogative of the council of the City Government).

It should also be mandated to publish budget and account documents as citizens should know how the public money is being used and operationalised for the development of the city. Hence, City Government should ensure financial transparency through publishing of annual budget and accounts.

3. Financial Ratios

| Ratios | 2017-18 | 2018-19 | 2019-20 |

| Annual Per Capita Growth | |||

| Total Income | -2.14 | -2.28 | 1.42 |

| Tax Income | 3.70 | 24.55 | 3.85 |

| Non Tax Income | 42.95 | -7.91 | -6.97 |

| Property Tax | 0.12 | NA | NA |

| Total Expenditure | -22.02 | 7.25 | -6.00 |

| Revenue Expenditure | -4.33 | 8.99 | -5.46 |

| Capital Expenditure | -43.97 | 3.56 | -7.21 |

| Ratios | 2017-18 | 2018-19 | 2019-20 |

| Percentage Share of | |||

| Revenue Income to Total Income | 57.88 | 63.59 | 63.12 |

| Own Source Revenue to Total Income | 36.58 | 43.08 | 43.04 |

| Tax Revenue to Total Income | 25.89 | 33.00 | 33.79 |

| Property Tax Revenue to Total Income | 17.96 | NA | 24.03 |

| Property Tax to Own Source Revenue | 49.09 | NA | 55.85 |

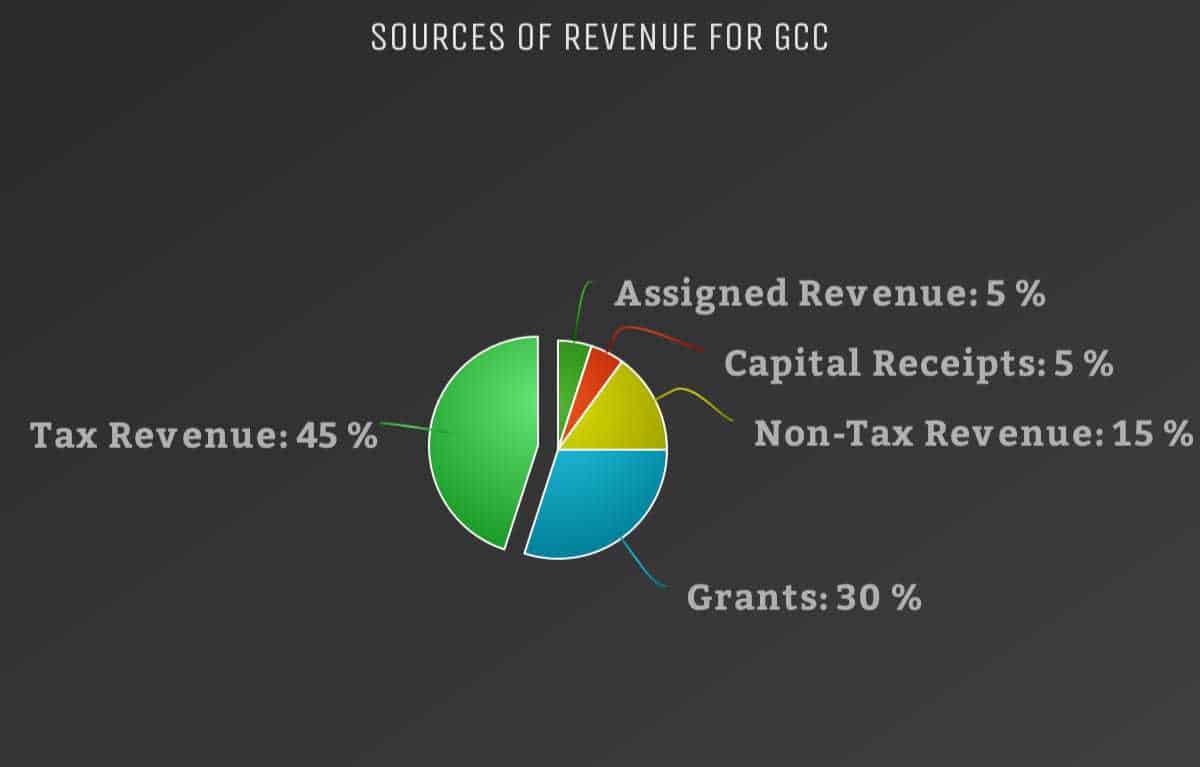

Greater Chennai Corporation (GCC) saw a drastic per capita growth in Tax Revenue Income in the year 2018-19 of 24.55 from a 3.70 in 2017-18. But the growth fell to 3.85 the very next year in 2019-20. Even though the rate of growth varies across years, Chennai has a positive growth for per capita tax revenue income. Chennai has seen a negative growth in Capital Expenditure. Capital Intensive projects act as an asset to the city and should be undertaken for the development.

Ratios for Revenue income to Total Income in Chennai have a positive growth from 2017-18 to 2019-20. Tax Revenue Income to Total Income has increased consistently from 25.89 to 33.79. Due to lack of property tax data for 2018-19 and 2019-20, the growth of property tax cannot be analysed.

Read more: Increasing property tax can be a gamechanger for city: DC, Revenue & Finance

Greater fiscal autonomy is necessary

In the present governance structure, city governments depend on the state and central government for funds and resources. For the city government to be independent and financially secure, fiscal decentralisation is very crucial. One such method to ensure devolution of power is by providing city governments independent authority to introduce new taxes and revise tax rates/charges.

Greater Chennai Corporation does not provide Property Tax values in all its budget documents. Property Tax is the main source of revenue generated for the city governments. Therefore, transparency in the property tax values can indicate the rate of growth and also direct different policies or strategies for extensive revenue generation. In addition to it, publishing Credit Rating in the financial statements/budgets illustrates the transparency and accountability of the city government.