Every afternoon, Nanda Kumar makes a difficult choice. He parks his bike outside his home in Chennai and suspends work, losing up to ₹800 a day. The 27-year-old Ola and Uber rider isn’t on a break for leisure, though. A brutal heatwave and a recent heat stroke that landed him in the hospital for two days cost him over ₹10,000 in medical bills and lost wages. Since then, he has been forced to stay off the roads during the afternoon hours. “I can’t ride between 12 and 4 pm in the summer months. The heat is just unbearable,” he says.

So, what about the loss of earnings? The concept of heat insurance is new to Nanda Kumar but when it is explained to him, he feels it is the need of the hour. A solution for lakhs of gig workers, who are losing work in summers. “Let us not forget that heat stroke cases are rampant among us,” he added.

Forget heat insurance, Nanda Kumar says there is no mechanism to reach out to Ola and Uber to share concerns or register complaints. “For a six kilometre ride, we are paid anywhere between ₹60–70. It would be great if the amount is increased to ₹100 for those riding during peak heat hours,” Nanda Kumar said.

Read more: More heat, less business: Street vendors struggle as temperatures soar in Mumbai

In Bengaluru’s Mahadevapura, Krishna Kumar, a street vendor selling ice apples, dreads this summer more than ever. What was once a bearable season has become punishing. By noon, his eyes go dry in the heat, his skin is singed and body drained, forcing him to wind up early. Heading home comes at a cost: he loses half a day’s income, every single day.

With no access to formal credit, Krishna has turned to private moneylenders. “Which bank gives us loans?” he asks. “To make ends meet, I have borrowed ₹50,000 from a local financier. I now pay ₹5,000 every month just in interest.”

Heat insurance to the aid

For the informal workforce, for whom the scorching summer streets are the workplace, heat insurance can offer some respite, if not emerge as a game changer. Hasumathi’s tale shows us how.

For 50-year-old Hasumathi Kailesh Kumar Parmar, a catering assistant in Ahmedabad, the month of May, with the wedding season in full swing, is a time of opportunity. It is also one of the hottest months in India, when a high number of heat stroke cases are reported.

Hasumathi never missed work though — dehydrated and sweating in the kitchen, she would try to make hay while she could. But over the past two years, skipping work for at least four days in May has become the norm, as working in the kitchen in the sweltering heat has brought on diarrhoea, heat boils and infections.

May has thus turned into a month of mounting costs — both on account of medical expenses and the lost income from the days she is forced to take off. But in some respite, a heat insurance initiative from Mahila Housing Trust — an organisation strengthening grassroots collectives of women in the urban informal sector — has covered part of her losses. Hasumathi paid ₹354 as the yearly premium for the parametric heat insurance to Mahila Housing Trust.

To develop this insurance, MHT partnered with Global Parametrics, an organisation specialising in climate risk solutions, and Go Digit Insurance, the underwriting firm. Since this is a pilot project and building insurer confidence takes time, insurance broker Howden India stepped in to subsidise the premium amounts on behalf of the insurers.

“This is a seasonal insurance policy, running from March to June, and follows a two-tier payout model. In Ahmedabad, if the threshold temperature of 43.7°C is breached for two consecutive days, the insured person receives ₹750. If the higher threshold of 44.1°C is breached for two consecutive days, they receive ₹1,250. Each beneficiary can receive both payouts once per season, with the maximum benefit capped at ₹2,000,” says Bhavna Maheriya, program manager of Mahila Housing Trust.

In Vadodara, Mahila Housing Trust has set the maximum temperature threshold at 43.6°C for two consecutive days. In Surat, it has to breach 37.8°C for two consecutive days for insurance payout to be initiated.

Last year, in Ahmedabad, with temperatures crossing the lower threshold only, 2,000 women such as Hasumati received a sum of ₹750 each, totalling to ₹15 lakh. “I received ₹750 last year; this money makes a lot of difference in compensating for the days when I miss work,” Hasumathi tells us.

What is parametric insurance?

According to an article from World Economic Forum, parametric insurance is a type of insurance that pays out when a predetermined event occurs, such as a certain temperature being reached or a certain amount of rainfall falling.

A climate risk measure, parametric heat insurance acts as a safety net for poor communities working in extreme heat—those who have contributed little to climate change but bear the brunt of its impact. Temperature triggers based on historical local weather data serve as the benchmark for payouts in this type of insurance.

Self Employed Women’s Association (SEWA), another organisation covered 21,000 women working in the informal sector in 2023 under parametric heat insurance. What started off as an item-based insurance providing large umbrellas for street vendors, solar lights for salt pan workers and water jugs for all informal work groups, developed into monetary insurance last year.

“Our members pay ₹300 as premium for the heat insurance. In Ahmedabad, if the maximum temperature crosses 43.6°C for two consecutive days , a common payout of ₹400 is issued. In a week, if the temperature is above 43.6°C for three consecutive days, they get an additional ₹300. The maximum they can get through this programme is ₹2,100,” says Anisha Bagban, Secretary, SEWA, adding that the programme covered a lakh women from seven cities of India.

Heat insurance in Indian cities: Policy-level adaptation needed

Despite the demonstrated benefits of schemes such as the above, parametric insurance for vulnerable groups exists only at an organisational level, with little to no involvement from local, state or national governments.

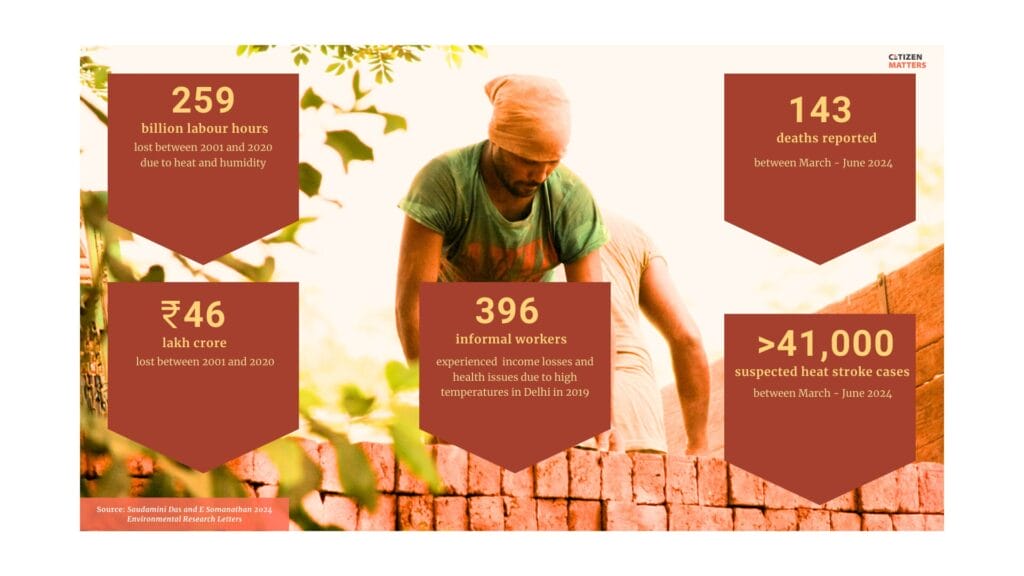

Every summer, like clockwork, cities roll out the same cycle of relief measures: heat action plans, water distribution drives and temporary shelters. Crores are spent, yet these efforts fail to address the economic impact of heat stress.

A report released by Sustainable Futures Collaborative, a Delhi-based organisation working on climate change, environment and energy, finds that long-term actions such as developing insurance cover for lost work has been missing from all the nine cities where the research was conducted.

“Parametric heat insurance was started in Ahmedabad by a few private entities for informal women workers but does not feature in the heat action plans in Indian cities,” says Tamanna Dalal, one of the authors of the study. She foresees the private players playing a big role in this field for a few years.

However, none of the four cities Citizen Matters checked — Chennai, Thane, Bengaluru and Ahmedabad — are making any progress towards that. Those who are at the helm of heat action policy are in fact often oblivious to the concept.

Experts consider it feasible to implement state-level parametric insurance schemes for climate risks, citing Nagaland as a pioneering example. In 2020, Nagaland became the first Indian state to introduce a parametric insurance programme covering excess rainfall, wherein it provides financial assistance based on predefined rainfall thresholds.

Heat insurance can be incorporated into the policy in multiple ways, say experts. “Either the disaster management departments or the welfare boards for workers can adopt it as a policy. The government portal, e-Shram, can be used to identify the workers,” says Rashim Bedi, Senior Coordinator, policy intervention, SEWA.

Read more: Inclusivity is pivotal to measures against heat, says urban planner Jaya Dhindaw

City level or national level?

City level action plans are usually considered the best bet for effective heat insurance as the temperature triggers, humidity levels and the nature of heat differ from one city to the other. But Ulka Kelkar, executive director-climate, World Resources Institute (WRI) India differs in her opinion.

“Heat insurance should be implemented at a national level to have a wide impact. When more people pay premiums, the risk is spread across a larger pool. Since not everyone will claim at once, the pooled money can easily cover those affected, making payouts sustainable for insurers,” says Ulka.

Otherwise, she fears that the provider will either increase the premium amount or cancel the insurance scheme altogether. During the recent California wildfires, for example, there were reports of insurance companies adding additional conditions, increasing premiums, or even suspending it altogether in some cases.

Governments must play a key role as purely commercial insurance models will not be financially sustainable. “Private insurance should be supported by public sector backing through a layered funding approach,” explains Ulka, “The first layer involves private insurance, followed by reinsurance as the second layer, also provided by private entities. The third and final layer consists of government funds and contributions from international financial institutions.”

There are also behavioural and perceptual barriers to tackle in a country where insurance is still seen more as a financial product than a tool for risk protection. “Most people lack even basic life insurance. Vulnerable communities have the least capacity to insure themselves. Non-life insurance is mostly limited to motor vehicles, while disaster-related insurance remains negligible,” says Dr Saon Ray, visiting professor, Indian Council for Research on International Economic Relations (ICRIER), New Delhi.

Saon refers to a possible public-private partnership model, wherein the risk is shared between the state and insurers, similar to Japan’s earthquake insurance scheme. In that case, the government and private companies co-finance payouts, ensuring financial resilience against disasters, reducing the fiscal burden on individuals and municipalities while improving climate risk management.

How can heat action plans be more effective?

- Include partnerships with insurers to offer parametric heat insurance for informal workers, triggered by temperature thresholds.

- Create provisions in city budgets to compensate workers who lose income during extreme heat days.

- Use heat alerts to trigger rest periods or work stoppages, along with temporary financial support.