If one were to compare the national economy to the human body, highways can be considered the arteries. Like clogged arteries which can be life-threatening, poor roads can derail economic growth. Planning and execution of highway projects have several other implications related to safeguarding the interest of the consumer, environmental impact, prudent contract management etc.

One way to be aware of issues of impropriety and poor performance in local government bodies and departments is to track the audit reports from agencies like the Comptroller and Auditor General of India (CAG).

This article is the sixth in the Series: Understanding Public Project Audits, by experts from the Indian Accounts and Audit Service.

The objective of this article is not only to highlight the lapses observed by audit in the construction of roads by the Karnataka Road Development Corporation Limited (KRDCL), but also to briefly introduce the readers to the norms, procedures and processes involved in road construction.

Karnataka’s highway projects

Karnataka has the second largest network of state highways, fourth largest overall road length and fifth-largest length of National Highways (as per the latest MoRTH report – Road Statistics 2017-2018). The KRDCL was established in July 1999 to construct, erect, build, develop, improve and maintain express routes and roads and bridges, sideways, and tunnels and to decide, levy and collect toll/service charges.

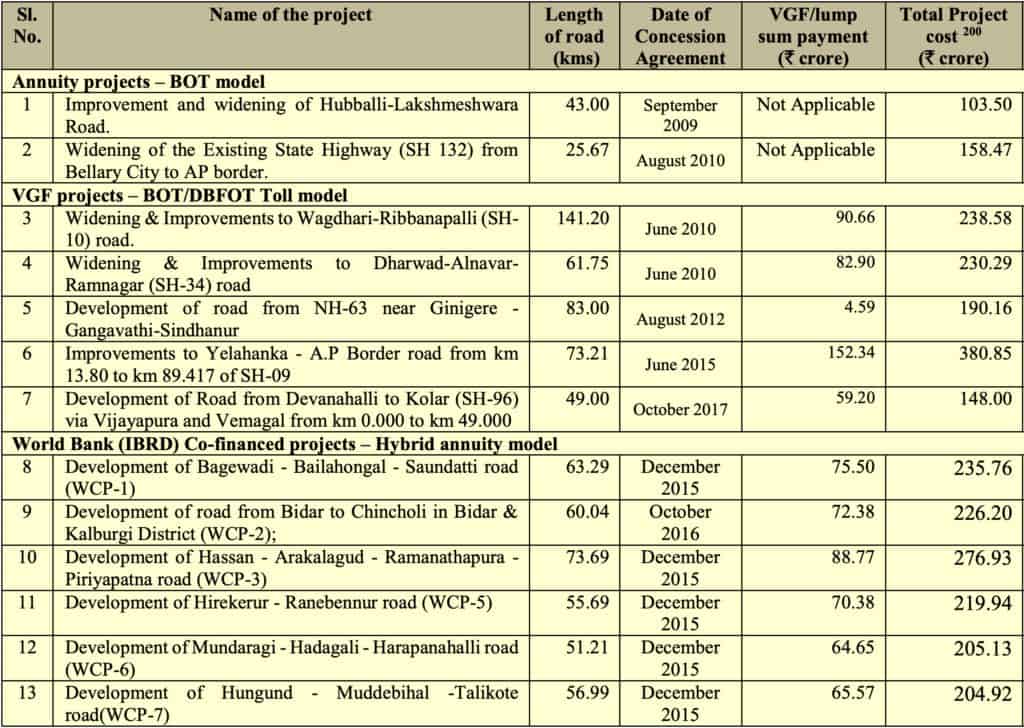

KRDCL has implemented 12 Private-Public Partnership (PPP) projects to build a total length of 788.74 km at a total cost of Rs 2,670.73 crore. The Office of the Accountant General–Audit II, Karnataka, conducted a performance audit of these projects to assess whether the conceptualisation and selection of PPP projects were in tune with the guidelines and also to examine the planning, implementation and monitoring aspects of the projects. The details of these projects are in the table below:

Audit findings are highlighted broadly under four different sections,

- Inconsistencies in the selection of projects

- Execution of projects

- Levy and collection of toll

- Operation and maintenance and Post-implementation monitoring.

The selection of the PPP model is a complex process which depends inter alia on factors such as financial resources, anticipated returns, value for money, risks involved, technological innovation etc. KRDCL executed six projects under World Bank Co-financing through a Hybrid Annuity model (Under this model, 40% of the total project cost was provided jointly by KRDCL and the bank, as a lump sum to the builder/Concessionaires. The remaining 60% of the cost was invested by the Concessionaires, which was reimbursable in the form of fixed semi-annuity payments during the concession period of eight years).

The selection of a PPP model is a complex process which depends inter alia on factors such as financial resources, anticipated returns, value for money, risks involved, technological innovation etc. KRDCL executed six projects under World Bank Co-financing through the Hybrid Annuity model.

Read more: How is it that roads in Electronics City have no potholes?

Issues in initiating highway projects

Inconsistencies in the selection of projects for execution as well as the PPP model were noticed as indicated below:

- VfM – Value for Money (VfM) assessment needs to be carried out to judge whether a PPP is likely to offer better value than traditional procurement. Two out of six projects, which had negative VfM, were approved at higher semi-annuity. This resulted in an additional outflow of Rs 80.16 crore over the concession period of eight years.

- Equity IRR – As per the norms of Union Ministry of Road Transport and Highways (MoRTH), a bid is acceptable if Equity IRR (used to calculate return on investments after accounting for the debt financing) is up to 18%. If Equity IRR exceeds 18%, the project needs to be bid on Engineering, Procurement and Construction (EPC) mode. The Steering Committee/PGB, while approving (July 2015/August 2015) the projects under PPP, considered only VfM as the criterion for accepting or rejecting the bids, without considering Equity IRR.

- Traffic volume – The norms also stipulated that if the traffic volume is less than 5,000 Passenger Car Units (PCUs), the project was required to be taken up on EPC mode. The traffic volume of the six projects as per the traffic survey conducted (September/October 2013) by KRDCL at 13 locations/chainages ranged between 1,630 PCUs and 4,508 PCUs. The actual annual toll revenue from these six roads was only about 25% of the estimated Rs 55.62 crore (December 2015) i.e. Rs 13.04 crore (December 2019). The projects were unviable and KRDCL had to depend on state budgetary support for repayment of the project loans.

Note:

VfM = Net Present Value (NPV) of semi-annuity quotation by successful bidder – semi-annuity threshold determined.

Semi-annuity is the amount that is to be paid half-yearly to the successful bidder (Concessionaire) over the period of concession based on the quotes accepted.

Read more: What fixing our own roads taught us about local democracy

Project execution – Unjustified toll collection

In the case of BOT projects, i.e Built Operate Transfer, toll can be collected by the concessionaire on the declaration of the Provisional Commercial Operation Date (PCOD) i.e after completion of 75% of the total length of the highway.

The PCOD for the Yelahanka–AP border road was issued in September 2018 on completion of 55.522 km (75.76 per cent) of the total length of the highway project and the Concessionaire commenced collection of user fees. However, intermittent stretches for a total length of 16.480 kms were pending completion due to incomplete land acquisition (May 2019). Incomplete stretches were observed every one to two kilometres resulting in a sub-optimal experience for the user. Thus toll collection lacked justification.

The Dharwad-Alnavar-Ramnagar road with a length of 61.75 km was declared open for provisional commercial operation with effect from August 2013. The scope of the project included the construction of three Rail-Over-Bridges (ROB) which were not completed even as late as December 2019. Consequently, 3.13 km of approach road to the ROBs was not completed and the users were deprived of a hindrance-free road, despite paying toll since August 2013.

Incomplete safety requirements

KRDCL and the Concessionaires failed to perform their obligations with respect to safety requirements. The safety audit conducted (December 2018) during the operation and maintenance period in respect of Wagdhari-Ribbanapalli road made certain important recommendations for rectification, viz. strengthening of shoulders on either side of the road, improving the capacity of identified junctions and footpaths, signages, road safety devices and road markings, and improvement to existing truck lay bay by constructing a median to bifurcate within the main carriageway. There was nothing on record in support of implementation by KRDCL/Concessionaire of the above recommendations.

Undue advantage to concessionaires

As per the terms of the Concession Agreement (CA) (Article 16), if the Concessionaire fails to complete any construction work on account of force majeure or for reasons solely attributable to KRDCL, the Concessionaire was required to pay 80% of the sum saved therefrom to the safety fund maintained by KRDCL within 180 days of the project completion date.

Audit observed that in two projects, KRDCL removed certain works from the scope. However, no action was taken to finalise the cost of de-scoped works in respect of the Bellary City-AP border project, while orders on change of scope were not issued in respect of the Darwad-Alnavar-Ramnagar road. This enabled the Concessionaires to evade payment to the safety fund. The Concessionaire of the latter project was required to remit Rs 32 crore to the safety fund. In the Yelahanka-AP border road, though there was a reduction in length of Right of Way (ROW), KRDCL did not take action to de-scope the works.

The Ministry of Road Transport and Highways (MoRTH) issued (November 2001) directions for use of fly ash in the construction of road/flyover embankments, especially in the areas where fly ash is available in plenty. The Ministry of Environment, Forest and Climate Change (MoEF & CC) also directed (November 2009) that no agency, person or organisation shall, within a radius of 100 km (revised to 300 km in January 2016) of a thermal power plant, undertake construction or approve the design for construction of roads or flyover embankments with topsoil. The audit observed that the use of fly ash was not considered in three projects, viz. Bellary City-AP border, Ginigere-Gangavathi-Sindhanur, and Bidar to Chincholi road though they fell within the limits of the specified distance of Raichur Thermal Station.

Levy and collection of toll at highways

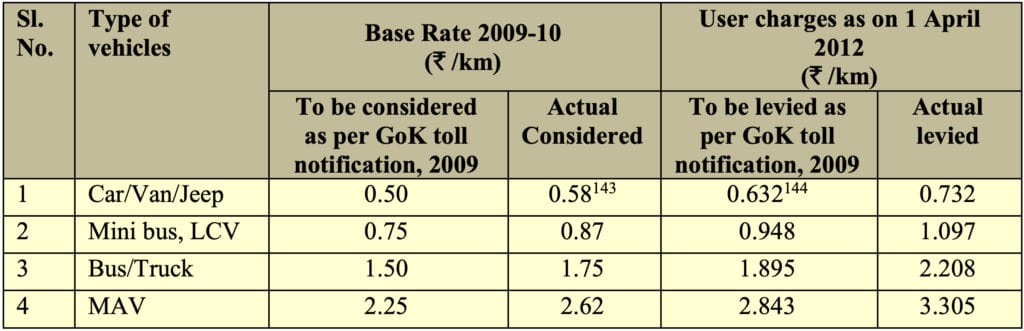

As per Karnataka Private Investment Project (Road toll or User fee determination of Rates and Collection) Notification, 2009, the base toll rates of 2009-10 as given in the notification were to be increased every year from April 1st on the basis of Wholesale Price Index (WPI).

The audit observed that the toll rates were determined as per the model notification annexed to the CA, which were higher than that in the approved GoK notification. Further, the model notification allowed for an annual increase considering the Wholesale Price Index (WPI) and an increase of an additional 3%, whereas the said notification allowed only for an annual increase on account of WPI.

The toll rates leviable as per the GoK toll notification, 2009 and the rates actually levied as per the model notification in respect of Wagdhari-Ribbanapalli road are indicated in the following table:

A similar method was followed for collecting toll rates for the Dharwad-Alnavar-Ramnagar road.

Thus, fixation of toll in violation of the Toll Notification, 2009 resulted in excess and recurring burden on users and extension of undue benefit to the Concessionaires.

Audit quantified the excess user fee collected from the users of two BOT projects, Wagdhari-Ribbanapalli road (April 2018 to December 2018) and Dharwad-Alnavar -Ramnagar road (April 2018 to March 2019) based on available data which worked out to Rs 6.24 crore and Rs 1.24 crore respectively.

As per the GoK toll notification 2009, levy of user fee is applicable only for two-lane roads with a width of 7-metre carriageway and above. The total length of the Dharwad-Alnavar-Ramnagar road was 61.75 kms, which included the length of 23.20 km passing through the reserve forest area having a carriage width of 5.5 metres. However, the Concessionaire was allowed to levy and collect toll from the users for the entire stretch of 61.75 km instead of restricting it to 38.55 km (excluding 23.20 km). This was in violation of GOK’s toll notification.

KRDCL also did not take action to de-scope the work of reduction (estimated at Rs 10.49 crore) in width from seven metres to 5.5 metres for this stretch of 23.20 km. The excess collection of toll for 23.20 kms, which had a carriage width of 5.5 metres, worked out to Rs 1.41 crore from April 2018 to March 2019. This excess toll which will be collected up to December 2040 is an unwarranted burden on users but benefit to the Concessionaire.

Operation, maintenance and post-implementation monitoring of highway projects

The CA concluded by KRDCL for Annuity/VGF projects stipulated that the Concessionaire should carry out periodic preventive maintenance to ensure safe, smooth and uninterrupted flow of traffic on the Project Highway during the concession period. In five projects, KRDCL had no system in place either to ensure that the Concessionaires complied with these conditions or to invoke contractual provisions and recover such costs from the Concessionaires. Failure to maintain the roads as per maintenance requirements had not only caused inconvenience to road users but also deprived them of better value for money and enhanced quality of services expected to be provided under PPP.

This also resulted in undue benefit to the Concessionaires as KRDCL failed to invoke the terms of the Concession Agreement.

M/s GVR Infra Projects Ltd, Chennai, which is the Concessionaire for three projects, had become insolvent. The condition of the Dharwad-Alnavar-Ramnagar road deteriorated, as the design life of the upper bituminous layer was only five years. However, the Concessionaire did not take action for overlaying the road with bituminous concrete after the completion of five years from COD (due in August 2018).

Other projects too faced similar problems. No action has been taken for renewal of the wearing course for Wagdhari-Ribbanapalli road even beyond the due date (January 2018). The renewal of wearing surface of Bellary City-AP border road pavement was done in December 2018 against the due date of March 2017, i.e. 22 months after the due date.

The issues highlighted above are illustrative of the common issues that are observed in road projects executed by various other agencies – state and central – under different models like Build-Own-Operate (BOO), Build-Operate-Lease-Transfer (BOLT), Design-Build-Operate-Transfer (DBFOT), Lease-Develop-Operate (LDO), Operate-Maintain-Transfer (OMT), etc.

The Audit Report was presented to the state legislature on February 3rd, 2021 and can be accessed here (English and Kannada versions)

[The authors are from the Indian Audit & Accounts Service. Views expressed are personal]

Good job.

Concentrate on O&M and MM.